If you haven’t already, join 9,574 other business lovers and subscribe for free:

Today’s post is sponsored by Stratosphere.io. It’s a financial data platform that we use and it’s awesome for gathering and visualizing financial data for any company you’re researching.

Get started researching on the Stratosphere.io platform today, for free. And you can use the promo code: investingcity for 25% off your first year.

Real quick, before we dive in, I’ve been testing out Substack Notes, and would love for you to join me there!

Notes is a new space on Substack to share links, short posts, quotes, photos, and more. I plan to use it for things that don’t fit in the newsletter, like work-in-progress or quick questions. Ok, let’s jump into today’s breakdown!

Adobe sells software for designers and marketers. Its products are so popular some of them have become verbs (“I need to Photoshop that picture.”)

Here are the company’s trademarks:

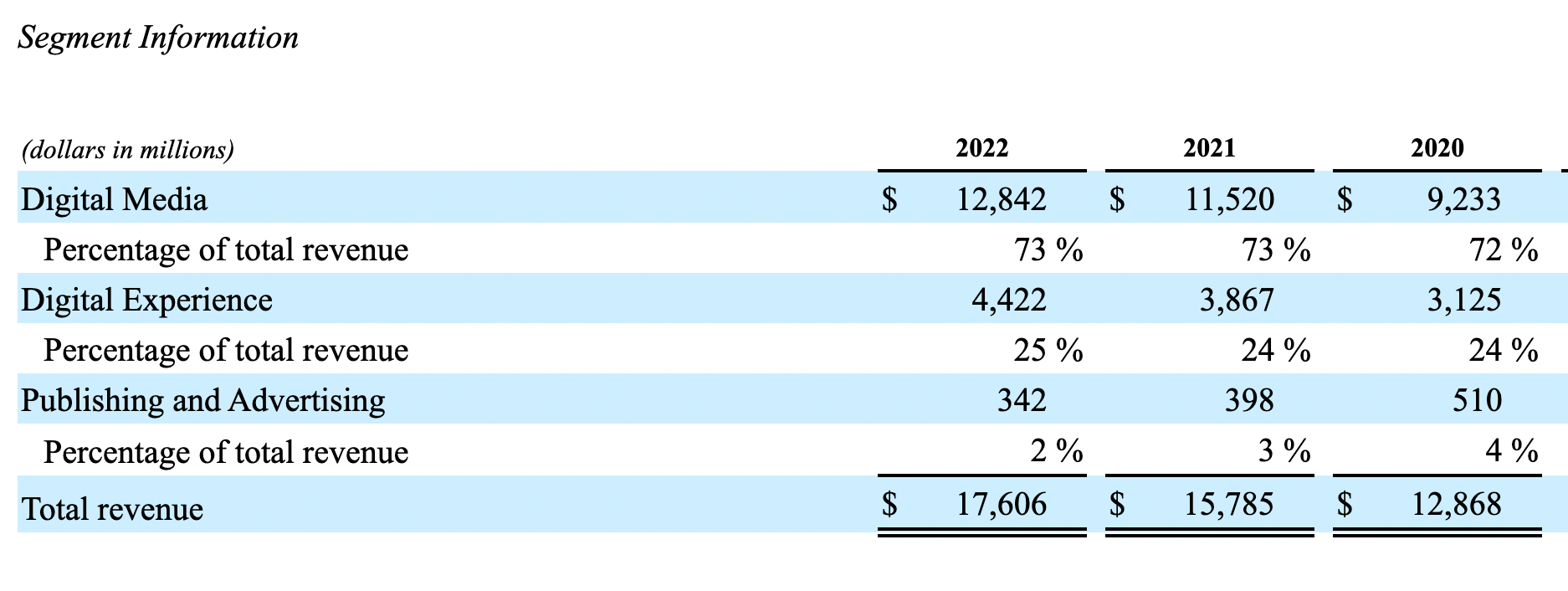

Adobe’s business is comprised of three segments:

Digital Media

Digital Experience

Publishing

Starting with the biggest segment, Digital Media includes the Creative Cloud, a bundle of professional software. Users can also purchase each product a-la-carte style.

Moving to Digital Experience, this segment is sold to enterprises looking for turn-key solutions for advertising and marketing.

And lastly, Publishing is the smallest segment, making up just 2% of overall sales.

Here is the revenue break-down for these three segments:

As you can see, Digital Media is the biggest segment by far, making up 73% of overall sales.

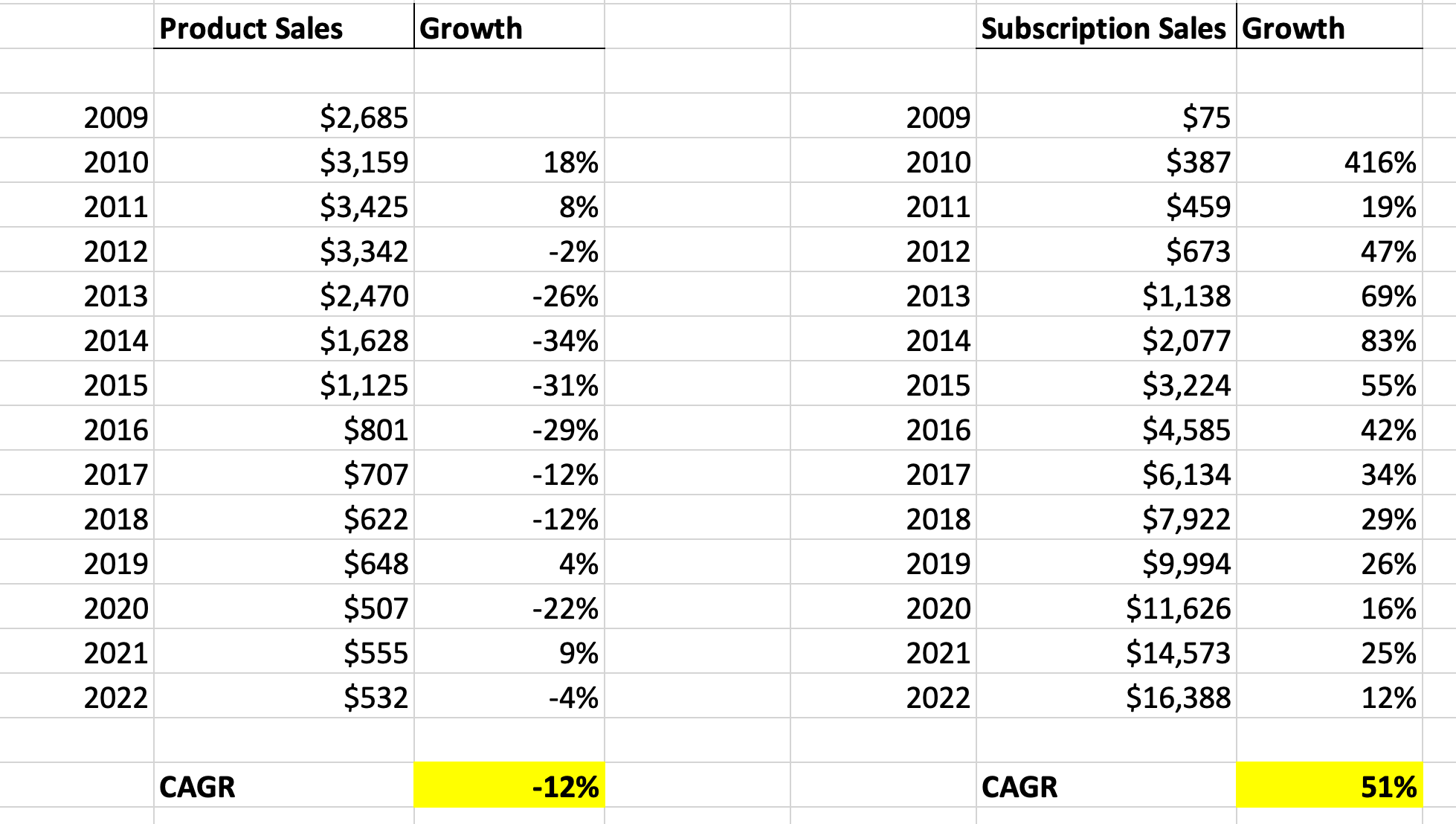

Now, let’s look at the business through its product delivery methods. In 2011, the company announced it was shifting to a SaaS model instead of a one-time licensing fee. Rather than customers buying Photoshop and being able to use it forever (without updates), customers could now purchase Photoshop on a monthly basis, lowering the initial costs and pricing in the cost of updates.

Initially, the company got a nasty response; 30,000 customers signed a petition to stop Adobe’s actions. But the company persisted. Here is how the Creative Cloud annual recurring revenue has trended since that point, growing at an astounding 52% CAGR:

Product revenues accounted for 81% of sales in 2011 but just 3% in 2022. On the other hand, subscription revenues went from 11% to 95% over the period.

Here’s a different look at this progression:

The combination of growing subscription sales and decreasing product sales led to strong overall growth as well.

Over the decade, product sales dropped off by about $2 billion but subscription sales added nearly $16 billion. A net gain of $14 billion led to strong revenue growth numbers.

What’s interesting is that overall revenue nearly declined on an absolute basis from 2011 to 2014. While the transition was well underway from license to SaaS, the nature of each consumption method warped the numbers. If lump-sum payments are replaced with monthly or annual payments, the overall revenue numbers will look much smaller. In the long run, visibility will be higher from recurring revenue but the early days of a transition make growth look funky.

Here’s what the transition did to margins:

Gross margins compressed a little bit because hosting a cloud-based product is more expensive. Paying cloud providers eats up some margin.

And operating margins suffered because revenue dropped off.

You can imagine what Wall Street was thinking at this time. In 2013, two years after the announcement of the transition, the company’s sales decreased 8% and EBIT margins went from 27% to 10%. That is a HUGE drop in earnings.

Just look at what the stock did over a five year period, ending in 2013. It was essentially flat.

That’s why it’s important to know what metrics to look for as an investor. In 2013, subscription revenue grew 69% and then 83% the next year. It really was the inflection point. Since then, the stock has risen about ten-fold. While it is easy to tell a story with hindsight, the point is that stocks rarely go up in a straight line.

Adobe is definitely a testament to this.

But even strong companies face challenges. The latest whirlwind surrounding the company was the $20 billion acquisition of Figma. While it’s clear that the company was going to overpay, I think it shocked some investors to more seriously assess Adobe’s competitive advantage. Figma’s browser-based collaboration process is just so different from how Adobe’s products work. Now, however, the Department of Justice is expected to block the acquisition, citing anti-trust concerns. On one hand, some investors are happy that the company is being forced to be disciplined and not spend three years of free cash flow on Figma. On the other hand, Figma will now continue to compete with Adobe, forcing them to innovate and not just sit back and collect that sweet, sweet recurring revenue.

Adobe is still the brand leader but leaders have a target on their back. Companies like Figma, Sketch, and even Canva are putting creative tools in the hands of everyone. This is good for consumers and it forces Adobe to innovate. 90% gross margins and mid-40% FCF margins are pretty great so Adobe will have to fight to maintain them, which really means that it’s likely margins won’t go much higher.

If you enjoyed this, please consider pressing that ♡ below to make it ♥️. This will help other readers find this newsletter. Thank you so much 😁

What Else We Offer

For self-directed investors: Dynasty Membership research service

Long-only fund: Infuse Partners

Other educational resources

Great Read! Thanks!

Well done, Ryan! Nice write up.