The Trade Desk

The dominant DSP

The Trade Desk created a software platform that enables advertising agencies to optimize their programmatic advertising among different digital channels. In plain English, The Trade Desk helps ad agencies spend their budgets more effectively.

Traditionally, ad-tech companies would act as a black box, profiting from the arbitrage between buying from publishers (websites, content creators, etc.) and selling to agencies (which help brands). The Trade Desk takes a completely different approach by focusing solely on the buy-side agencies. The value of this is that the company establishes strong, recurring relationships. The metric to watch is the retention rate, which measures customer churn, and it has been above 95% for the last decade.

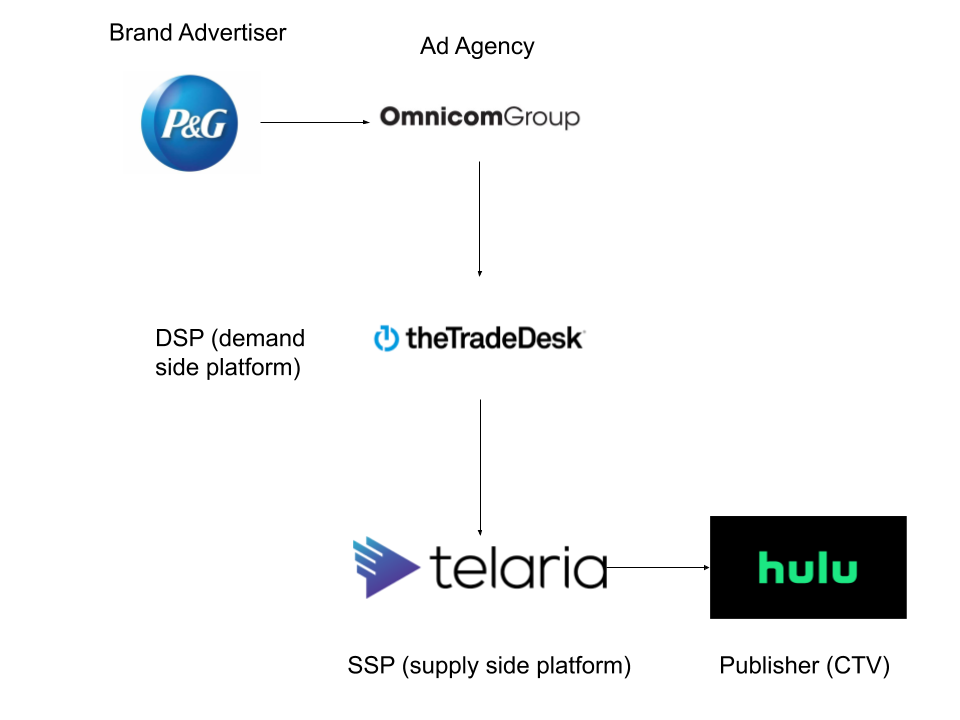

Below is a graphic of the complicated value chain in this industry. It starts with Proctor and Gamble wanting to make its advertising dollars go further. The marketing department approaches their advertising agency and the agency tells them about programmatic advertising and a specific DSP (demand-side platform) called The Trade Desk. Apparently the agency uses this platform for some other clients and the ROI has been amazing. P&G is sold and tries it out.

Going a little deeper, The Trade Desk sits in the middle between brands and agencies who need to buy advertising somewhere (buy-side) and publishers who need to monetize advertising inventory (sell-side).

Coming from the other side of the value chain, Hulu has ad slots it needs to fill for free users who sign up for the ad-supported version. It hires an SSP (supply-side platform) to manage these ad slots, ensuring it gets the highest CPMs (cost per 1000 impressions) and therefore, more revenue. Not all publishers utilize SSPs but most big companies will. The more ad slots that need to be filled, the more complexity.

So we have a clear market. The brand advertisers want higher ROIs on their ad budgets so they want to pay low CPMs. And the publishers, who sell the inventory, want high CPMs. The Trade Desk’s platform is an open environment that allows this traditionally opaque market to function at a high level.

To drill into the technology a little more, The Trade Desk specializes in what is called programmatic advertising. Rather than people going around, negotiating CPMs, the company’s platform allows ad agencies to buy inventory through its software program. To overly simplify, an ad buyer will set limits on what their client can spend, and then The Trade Desk will match that client with an associated publisher. At its core, The Trade Desk is really a data management platform that analyzes billions of impressions from hundreds of suppliers (ad exchanges, SSPs, publishers, and ad networks) and matches these impressions efficiently with its true customers, the ad agencies.

This is a process called real-time bidding (RTB). The Trade Desk’s platform is powered by software, which enables this whole process to function smoothly. It’s essentially providing liquidity to the digital advertising market so that the buy-side can have higher ROIs. In this way, it functions similarly to a stock exchange, enabling customers to get tight spreads for executing trades. Without liquidity, publishers can artificially inflate their potential ROIs for brand advertisers.

And this is exactly the case with “walled-gardens.” This is a term for a publisher that only allows advertisers to buy inventory through its own platform. For example, advertisers can only buy Meta ads through Facebook. In other words, The Trade Desk would have no access to Facebook’s inventory. Google is a tricky one. It’s actually a supplier and a competitor to The Trade Desk. Aside from being one of the company’s biggest sources of display advertising with AdSense, Google AdWords is pretty much a walled garden.

The big question around The Trade Desk has always been around this dynamic with Facebook and Google. Since both of these behemoths own such a large proportion of the overall ad market, where is The Trade Desk getting inventory from?

Fortunately, the company’s bread and butter is omnichannel: audio, video, display, native, and social across all devices. In 2019, clients spent about $3.1 billion through The Trade Desk’s platform and more recently, that numbers ballooned to $7.6 billion. This is still just over 1% of global digital advertising spend. Clearly, there is a lot of room for programmatic to take share. But that’s the thing, the company did $1.8 billion in revenues by servicing ~1% of the digital ad market. It doesn’t need an insane amount of inventory to be a pretty large company.

Imagine if programmatic grows twice as fast as digital advertising (the rates today) and The Trade Desk has 5% of the market in 2030. That’s $35 billion in gross spend on the platform.

The way the company actually reports revenue is on a take-rate basis; it’s about 20% of what ad agencies spend while using the platform. That might sound steep but it is really dependent on the ROIs the agencies are seeing.

The big risk, of course, is that The Trade Desk gets cut out as a middleman and the agencies become technically savvy enough to work directly with SSPs or publishers. There is a pretty low likelihood of this because agencies usually don’t work together too well. For instance, most agencies are made up of sub-agencies where it is hard to have a centralized technical team supporting each sub-unit. While it’s not impossible, the logistics of this are much more difficult than one might imagine. With the very biggest agencies, it’s more likely. I’ve heard a few cases of this so it’s definitely something to keep an eye out for. However, if programmatic dollars keep flowing into digital advertising and ROIs stay high, it shouldn’t be a problem.

The bottom line is that market power really matters here. The big brands with in-house programmatic capabilities will want to work directly with DSPs. The big agencies will want to cut straight to SSPs. And the big publishers will work directly with brands/agencies as a walled garden. Navigating all of these dynamics can be tricky when it’s still a relatively new space and there is a lot of growth. As The Trade Desk gets bigger it bodes well for its market power. As long as it continues to provide value, this company should be much bigger in the future.

Despite the market dynamics, one thing that is convincing brands is that the The Trade Desk enables them to use first-party data. For instance, the company has a strong relationship with Walmart, where they can plug in real consumer data so that The Trade Desk can target that type of consumer. We’re starting to see more and more of these relationships and the company even has its own identifier (UID 2.0) that replaces cookie technology so that consumers can remain anonymous but advertisers can still effectively target them. While the stock has always been expensive, the founder, Jeff Green, basically created the entire category and he has been quite prescient. For example, he said that Netflix would do advertising years ago when Hastings was very adamant that they never would. Green was saying it was simple math — as soon as Netflix subscriber growth slows down a bit, they will have to do advertising. Once again, the stock is expensive but I wouldn’t bet against Mr. Green.

How Can We Help?

Looking to become a partner in our long-only strategy?

Interested in advertising to more than 10,000 investors?